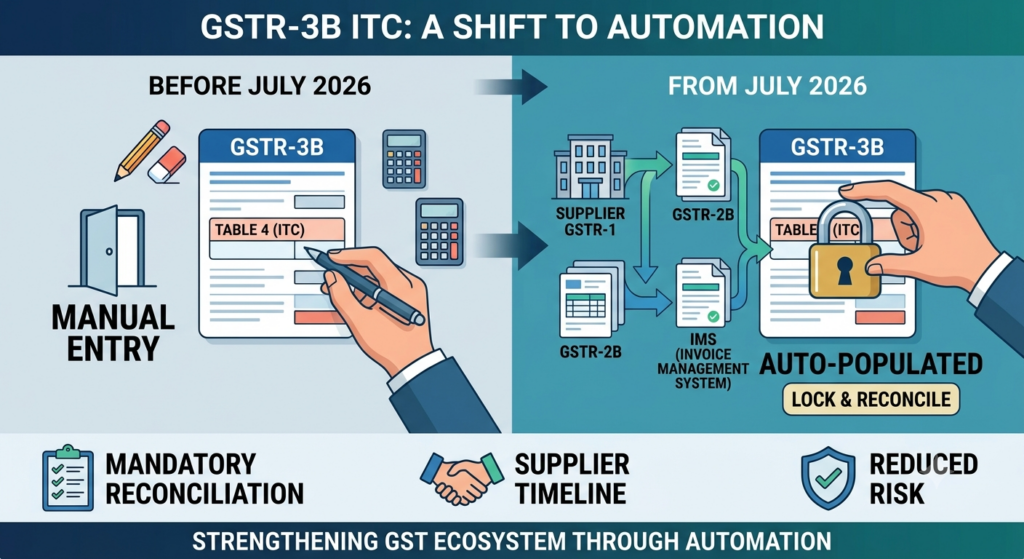

The GST compliance framework has taken another significant step towards complete automation. From the July 2026 tax period onwards, taxpayers will no longer be able to manually edit or amend the Input Tax Credit (ITC) figures in Table 4 of GSTR-3B. The ITC available for claim will be auto-populated based on the details reflected in GSTR-2B and the Invoice Management System (IMS).

What Has Changed?

Earlier, taxpayers had the flexibility to manually modify eligible ITC in GSTR-3B after carrying out their internal reconciliations. With the introduction of hard-locking, this flexibility is being withdrawn. The ITC reflected on the GST portal will become the basis for filing GSTR-3B, with little or no scope for manual intervention.

Objective of the Change

The Government aims to:

- Eliminate manual alterations in ITC claims.

- Ensure seamless matching of purchase data with suppliers’ returns.

- Reduce fraudulent or excess ITC claims.

- Strengthen transparency and improve GST compliance through system-driven validations.

Impact on Businesses

This change makes monthly reconciliation more important than ever. Businesses should:

- Reconcile purchase registers with GSTR-2B before filing GSTR-3B.

- Regularly follow up with suppliers to ensure timely and accurate filing of GSTR-1.

- Monitor invoices through the Invoice Management System (IMS).

- Resolve mismatches well before the due date to avoid loss or deferment of eligible ITC.

Key Takeaway

The era of manually correcting ITC in GSTR-3B is coming to an end. Taxpayers must shift their focus from correcting errors at the return-filing stage to preventing errors through timely reconciliations and supplier compliance. Robust internal GST controls and regular vendor follow-up will be essential for safeguarding Input Tax Credit and ensuring smooth compliance under the evolving GST ecosystem.