Introduction

The Goods and Services Tax (GST) regime has consistently evolved to strike a balance between facilitating ease of doing business and preventing tax evasion. While technology has significantly streamlined the registration process, obtaining GST registration has often involved detailed verification procedures, particularly for new applicants.

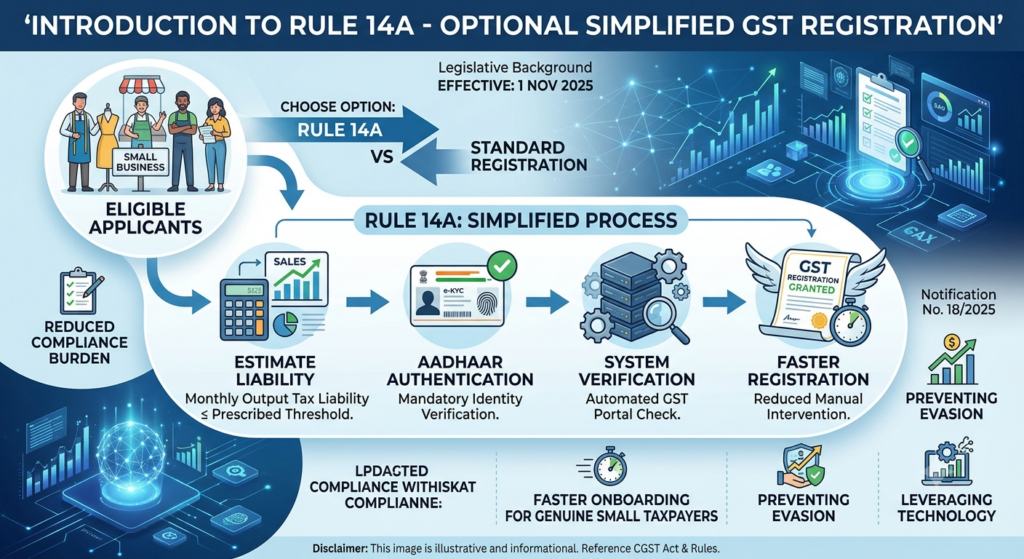

To simplify the registration process for small taxpayers while ensuring adequate safeguards, the Government inserted Rule 14A in the Central Goods and Services Tax Rules, 2017 through Notification No. 18/2025 – Central Tax dated 31 October 2025, effective from 1 November 2025.

Rule 14A introduces an optional, simplified registration mechanism for eligible applicants based on the expected level of tax liability and Aadhaar authentication. The objective is to enable genuine small businesses to obtain GST registration more quickly while allowing tax authorities to devote greater attention to higher-risk registrations.

Legislative Background

- Statute: Central Goods and Services Tax Act, 2017

- Rules: Central Goods and Services Tax Rules, 2017

- Inserted by: Notification No. 18/2025 – Central Tax

- Effective from: 1 November 2025

Rule 14A operates alongside the existing provisions governing GST registration and is intended to provide an alternative registration route for eligible applicants.

Objective of Rule 14A

The primary objectives behind introducing Rule 14A are:

- Simplifying GST registration for small businesses.

- Reducing procedural delays.

- Promoting voluntary tax compliance.

- Encouraging formalisation of small enterprises.

- Allowing tax authorities to focus verification efforts on higher-risk cases.

- Leveraging Aadhaar authentication and technology-based verification.

Applicability

Rule 14A applies only to eligible applicants opting for registration under the prescribed conditions.

It is not mandatory. Eligible taxpayers may continue to obtain registration under the normal registration process if they choose.

Eligibility Conditions

An applicant intending to avail the benefit of Rule 14A is generally required to satisfy prescribed conditions, including:

- Expected monthly output tax liability should not exceed the prescribed threshold.

- Aadhaar authentication should be successfully completed.

- Other conditions prescribed by the GST authorities should be fulfilled.

Failure to satisfy any of these conditions may require the applicant to undergo the regular registration process.

Understanding “Monthly Output Tax Liability”

One of the key concepts under Rule 14A is the threshold based on expected monthly output tax liability.

Output tax liability refers to GST payable on taxable outward supplies before adjusting any available input tax credit.

For example:

| Particulars | Amount (₹) |

|---|---|

| Taxable outward supplies | 18,00,000 |

| GST @18% | 3,24,000 |

| Output tax liability | 3,24,000 |

The determination of eligibility is based on the prescribed threshold under the Rule.

Aadhaar Authentication

Rule 14A places significant emphasis on Aadhaar authentication.

Successful Aadhaar authentication helps:

- establish the identity of the applicant;

- reduce fraudulent registrations;

- eliminate duplicate registrations; and

- enable quicker processing.

Applicants failing Aadhaar authentication may be required to undergo additional verification in accordance with the CGST Rules.

Registration Process under Rule 14A

The broad process involves:

- Filing the GST registration application.

- Completing Aadhaar authentication.

- Declaring the required particulars.

- Verification by the GST system.

- Grant of registration where the prescribed conditions are satisfied.

The process aims to minimise manual intervention for eligible applicants.

Circumstances Requiring Regular Verification

Even where Rule 14A is opted for, the Proper Officer may require further verification if circumstances warrant additional scrutiny in accordance with the applicable provisions of the CGST Rules.

Such verification may include examination of business premises, supporting documents, or other information necessary for determining the genuineness of the registration.

Advantages of Rule 14A

The introduction of Rule 14A offers several benefits:

1. Faster Registration

Eligible taxpayers may receive registration in a shorter timeframe.

2. Reduced Compliance Burden

The registration process is simplified for genuine applicants.

3. Improved Ease of Doing Business

New businesses can commence operations without prolonged registration delays.

4. Technology-Driven Verification

Reliance on Aadhaar authentication enhances efficiency while reducing manual intervention.

5. Better Administrative Efficiency

Tax authorities can focus resources on higher-risk cases instead of low-risk applicants.

Practical Illustration

Example

ABC Traders expects the following:

- Monthly taxable turnover: ₹10,00,000

- GST @18%: ₹1,80,000

If ABC Traders satisfies the prescribed conditions, including Aadhaar authentication and other eligibility requirements, it may be eligible to opt for registration under Rule 14A instead of undergoing the standard registration process.

Compliance Considerations

Businesses opting for Rule 14A should:

- ensure that declarations made in the registration application are accurate;

- complete Aadhaar authentication promptly;

- maintain proper books and records;

- comply with return filing requirements after registration;

- intimate changes in registration particulars as required under the GST law.

Challenges

While the Rule is intended to simplify registration, certain practical challenges may arise:

- Interpretation of eligibility conditions.

- Aadhaar authentication failures.

- Technical issues on the GST portal.

- Transition to regular verification where required.

- Need for clear administrative guidance.

Frequently Asked Questions (FAQs)

Is Rule 14A mandatory?

No. It provides an optional registration route for eligible applicants.

Does Rule 14A exempt a taxpayer from GST compliance?

No. Once registered, the taxpayer must comply with all applicable provisions of the GST law.

Does Aadhaar authentication remain important?

Yes. Aadhaar authentication is a key component of the simplified registration framework.

Can the department undertake verification?

Yes. The Proper Officer may undertake verification wherever required under the CGST Rules.

Practical Tips for Businesses

- Verify eligibility before opting for Rule 14A.

- Keep Aadhaar details updated.

- Ensure consistency in PAN, Aadhaar, and business information.

- Preserve supporting documents.

- Monitor GST portal communications regularly.

Conclusion

Rule 14A represents another step towards digitisation and ease of doing business under the GST framework. By introducing a simplified registration mechanism for eligible taxpayers, the Government seeks to reduce compliance costs for genuine businesses while maintaining robust safeguards against misuse.

Businesses should evaluate their eligibility carefully, ensure complete and accurate disclosures during registration, and continue to adhere to all post-registration compliances under the GST law. Proper implementation of Rule 14A has the potential to improve taxpayer experience, encourage voluntary compliance, and enhance the efficiency of GST administration.

Disclaimer

This article is intended for educational and informational purposes only. Readers should refer to the CGST Act, the CGST Rules, relevant notifications, circulars, and judicial precedents, and obtain professional advice before acting on any matter discussed herein.